Secure Your Child’s Future with a $1000 Child Retirement Credit

On: January 28, 2026

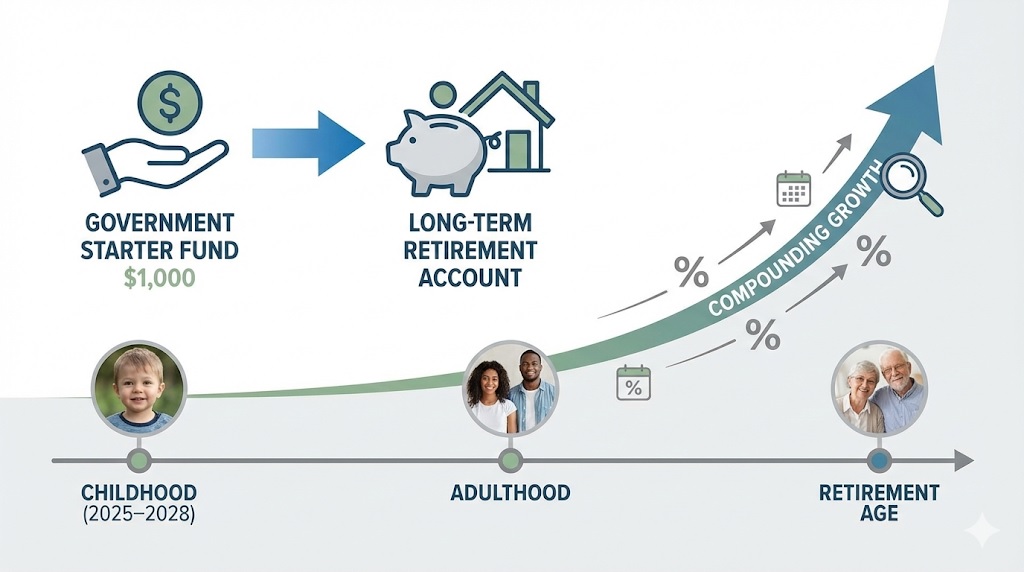

Young Americans have the potential earthquake in the financial landscape. The development of a new Child Retirement Account of $1,000 is the main suggestion of the Trump campaign, which has received great recognition. This program has also been colloquially referred to as Trump Accounts in the media, and its purpose is to provide every child born between 2025 and 2028 with a potent jumpstart to building lifelong wealth.

What are these accounts, though, how they operate, and how can parents make the most of this opportunity? This guide will de-jumble all information required about this new proposed retirement savings vehicle.

What is a Trump Account?

The main concept is simple: for each child born in the United States during the period of 2025-2028, the federal government would place a sum of 1,000 dollars in a separate and limited savings account for retirement savings. This is not a checking or regular savings account; it is a long-term investment vehicle that will increase tax-free over the decades.

The aim is titanic: to assist in financing a safe retirement for an entire generation and start tackling the looming retirement disaster. Assuming a compound growth of 40-50 years, it may be possible that the same amount of one thousand dollars as an investment in a seed may turn out to be a healthy, sizable nest egg by the time the child grows to retire age.

Key Features You Must Know About

This is important in order to maximize this advantage by understanding the mechanics behind it.

a) Eligibility Criteria

The proposal is only open to children who are born between January 1, 2025, and December 31, 2028. Its retroactivity does not cover children born prior to this period.

b) What Should Be the Initial Deposit?

The government contributes in the form of the first 1000 dollars. Parents do not have to phase out of income; the credit is universal among eligible newborns.

c) Account Structure

The funds would be invested in a limited investment account, such as a Roth IRA or 529 plan. This would be invested in various conservative/growth-oriented investment choices ( consider broad market index funds or target-date funds).

d) Restrictions

This is the vital element. Until the child is old enough to retire (probably about 591/2, similar to the existing regulations of IRA), the child is not allowed to obtain the money. This makes the power of compounding a lifetime pill.

e) Tax Treatment

The proposal would increase the accounts’ tax-free status, and also the qualified withdrawals in case of retirement would be tax-free, a mammoth benefit.

f) Contribution from the Parents

The best thing is that the parents, relatives, and later the child would be permitted to add more money to the account with the annual limits. It is in this that the actual prospects of wealth acceleration lie.

How to Maximize Opportunities?

The gift amount of 1000 dollars is good, but with proactive management, the gift can turn into a financial legacy.

1. Try Not to Set and Forget

Although the account will automatically be invested, be informed. Investment options are to be reviewed on an annual basis. As the child matures, you may decide to modify the risk profile, but a long time horizon tends to favour growth-oriented investments.

2. Use Meaningful Gifts

Rather than buying the toys that he or she will outgrow, invite grandparents, aunts, and uncles to add to the account to play during birthdays or holidays. However, even minor and regular donations can be overpowering.

Contributing only $50 a month since birth may lead to over 100000 at age 65 (assuming it earns 7 percent per year), in addition to the increase in the initial amount of 1000.

3. Financial Teaching Tools

When your child is mature enough, take this account as a practical, financial education. Prove them the statements, clarify the growth of the compounds, and explain why long-term investing is so important. This practical report is a valuable lesson in itself than any book.

4. Plan Your Contributions

Provided you can afford it, put up a small monthly donation. Automating even 25 a month transforms this stagnant gift of a dynamic savings habit that will accumulate value over the years.

5. Keep Records

There are high chances that you will be the custodian of the account until the time when your child becomes an adult. Keep detailed accounts of all donations (non-government ones in particular) to have them at hand when needed or to be able to prepare tax returns.

Considerations and Potential Challenges

There are no policies that do not have their shades. Be aware of the following:

a) It is a proposal

At this point, this must go through Congress. Although such a campaign plank is critical, it is not yet law. Keep track of its current legislation.

b) Long-Term Lock-Up

The limited access is a two-edged sword. It will keep the money increasing so that you can retire; however, it is not available to access in case of emergency, college fees, or a first-time down payment. Those objectives will require other saving products in your family.

c) The Unknowns

The details of investment decisions, the maximum amount of contributions that the family members can make, the transfer regulations, and the actual regulatory body are yet to be determined.

The offered “Trump Accounts” is a new way of thinking about retirement and generational wealth in America. It will be a secure future in the financial lives of qualified children. It is an appeal to action to the parents, not merely to take the gift of 1,000 dollars, but to work on it.

Through contributing, interacting with the account, and utilizing it as the foundation of your financial independence as a parent, you can contribute to one day facilitating this new concept into the cornerstone of your child to achieve financial independence. It is not just a policy, but an invitation to join in assuring the future of your child, sixty years down the line.

FAQ

1. Who is eligible for the $1000 account credit?

The eligibility is restricted to already born children in the United States who belong to the period between January 1, 2025, and December 31, 2028. The $1000 deposit is universal and not based on the income of parents among the qualified newborns.

2. When can my child get the money?

The funds are limited until the age when the child retires, like the present rules on IRA (probably around 591/2). This makes sure that the investment is not touched for decades due to compound interest.

3. Is it possible to add more money to the account?

Yes. Further contributions by parents, relatives, and later by the child are allowed with restrictions per annum. This is the most important trick in developing the account to a great extent out of the seed amount of $1,000.

4. Is this a law?

No. This is only a Trump campaign policy proposal that is not an active law. This would have to be adopted by Congressional approval, and thus, details may vary.

5. Can we use the money for college fees or a house?

No. Retirement withdrawals are not allowed. The money cannot be accessed to pay other significant bills, such as education and a first house. Those goals should be in separate accounts (such as 529s) of a family.

800-900-4250

800-900-4250