Possible Action Plans to Halt California Wage Garnishment

On: December 9, 2025

The word comes, and a shiver of cold fear passes through you. A Wage Garnishment Order has been served upon your employer. You are now going to lose a sizeable portion of your hard-earned salary to a creditor.

The panic is not imaginary–this is not merely the inconvenience; this is a direct danger to your capacity to pay the rent, purchase groceries, and sustain the family.

But take a deep breath. Wage garnishment is not the last outpost in California. It is a big money occurrence, yet it is also a procedure with regulations, time limits as well as and above all, various methods to prevent it.

This guide will be your map to the quick fix, how to understand what collection actions to take, and how to use a professional aid to regain power over your finances.

Have a Basic Understanding of Wage Garnishment

A wage garnishment (or earnings withholding order) does not fall out of thin air. It is the last thing in a legal course of events. Someone who owes money to you has to have you sued and a court verdict against you. It is on the basis of that determination alone that they can then request that the court make an order compelling your employer to forfeit a part of your wages.

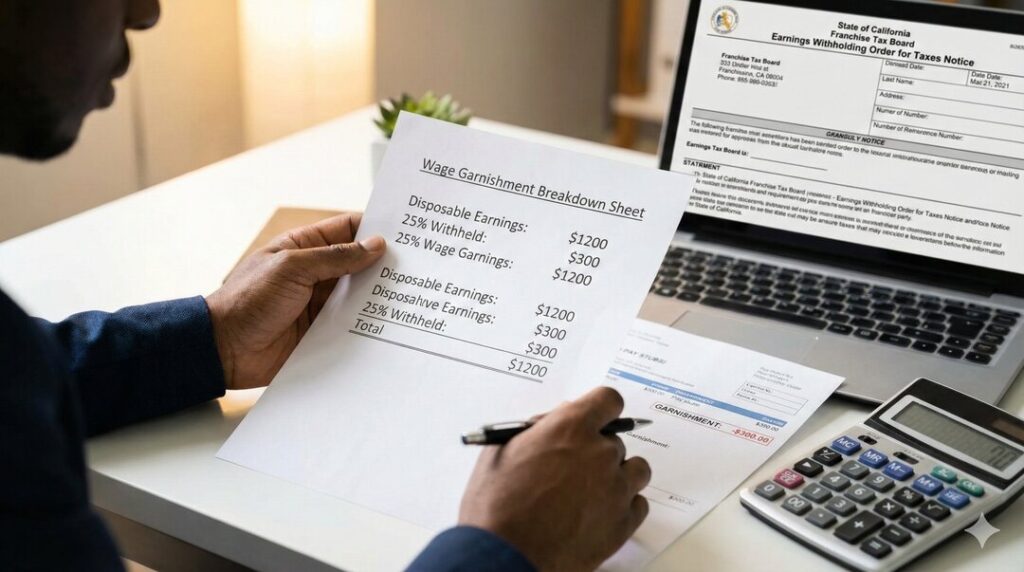

The garnish amount is also limited by law in California. In the case of the most common debts (credit cards, personal loans, medical bills), the garnishment is restricted to the lesser of:

- One quarter of your disposable income for the week, or

- The difference between your disposable earnings and 40 states of the minimum wage.

- This is to assist you in calculating the precise financial impact, which is the aim, yet what you need to avoid is it taking place at all.

Ways of Stopping Garnishment Instantly

When you are first notified, the clock begins to tick. Only a small amount of time is left to do it before the first deduction is deductible out of your paycheck.

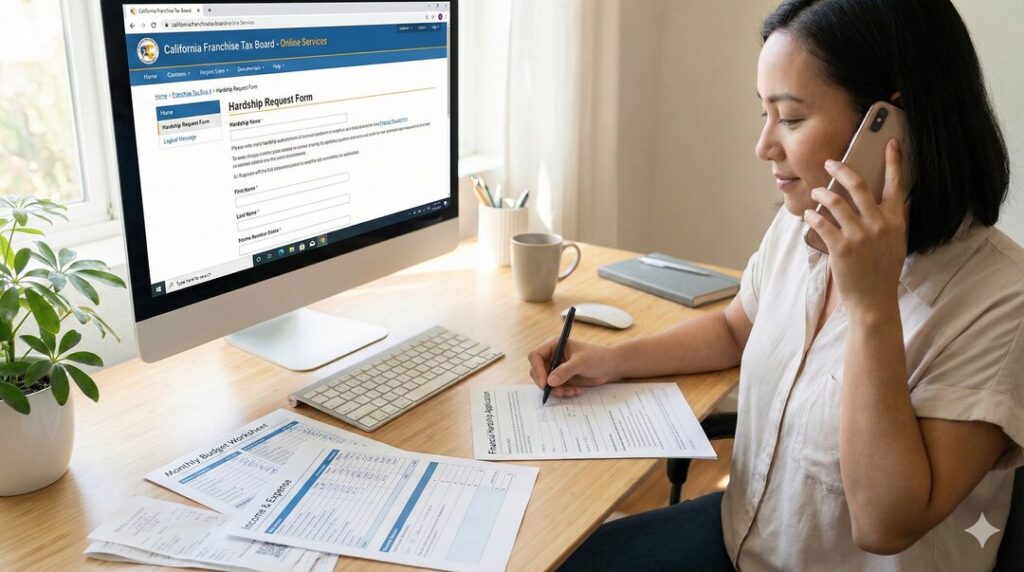

How to File a “Claim of Exemption”?

This is your ultimate weapon of short-term, temporary reprieve. In case the garnishment would reduce you to a level where you cannot make ends meet according to the basic living costs of your family, then you can submit this form to the court.

By submitting a Claim of Exemption, you are officially saying that your income needs to be legally safeguarded. The beautiful part? Making this claim automatically will, in the meantime, prevent the garnishment until the court has a hearing (typically within a few weeks) to resolve the issue. This will also leave you with time to strategize your next step.

What about the Stipulated Agreement?

Creditors generally like a predictable payment scheme to the inconvenience of a garnishment. Call the creditor or his lawyer himself and negotiate a payment amount that you could manage monthly.

In case you agree, you can make a formal agreement with the court to a so-called Stipulated Agreement, which will command garnishment to cease. Be sincere and true to your offer; it is not a bluff, it is a negotiation.

Understand the Threat of Levies and Liens

Although a wage garnishment is intended to go against your income, a judgment creditor has other weapons at hand. These will be like fuel to a fire to clear the debt at the base.

Bank Levy

The lender is able to freeze and steal your money in your checking or savings account. This may be even worse than a garnishment of wages, since this can drain out your emergency fund in one fell swoop.

Property Lien

The creditor may impose a lien on real property of which you are the owner, even on your home. This lien does not involve an immediate forced sale, but must be repaid before you can either sell or refinance the property, and cloud your title and your financial choices.

The garnishment of the wage is usually a way out of these other measures, because the creditor is already being paid.

How Powerful Is Professional Intervention?

It is daunting when one has to navigate through the legal system under the pressure of money. Professional assistance may come in handy here.

Hire a Professional

Hiring a bankruptcy attorney does not imply you are certainly going into a bankruptcy. To a large number of people, it is the only sure way of halting a garnishment. Once a bankruptcy case is filed, there is an automatic stay that has an immediate effect that stops any form of collection, even garnishments, levies, and lawsuits.

Depending on qualification, Chapter 7 type of bankruptcy might wipe the underlying debt off completely. In contrast, Chapter 13 may enable you to pay off some of it in a manageable court-approved plan.

Importance of a Debt Settlement Attorney

These are professionals who deal with debt, negotiating with creditors to pay less than the principal amount owed to them. They are aware of tactics and leverage points of the law that can result in a good one-time lump-sum settlement.

Credit Counselor

A credit counseling firm that is a non-profit organization can assist you in developing a budget and may place you in a Debt Management Plan (DMP). Although a DMP lacks the legal authority to halt an existing garnishment as bankruptcy, certain creditors, however, will give up the voluntary right to continue collecting once you are under an approved payment program.

Tips that Will Help You Take the Right Action

Act Now: Do not disregard the paperwork. Each day that you are waiting is a day that your paycheck will be cut down.

- Ready to demonstrate your financial difficulty. Collect pay stubs, bank statements, and a list of monthly expenses that you have to meet (rent, utilities, food, childcare).

- Any contract with a creditor should be in a written form, a formal, signed agreement that should be registered in court. The verbal promises cannot be enforced.

- In California, a certain group of income is completely exempt from garnishment, which includes social security, SSI, SDI, and Veterans Benefits. In case your bank account has this guarded money, you may oppose a charge.

California wage garnishment is an uphill task, but one that can be stopped. The way to ease the situation is to respond promptly and decisively. So that, whether you claim an Exemption, negotiate a settlement, or even obtain the mighty shelter of bankruptcy, you have a choice. Don’t let panic paralyze you. Get back control, consult a professional, and put financial bleeding to an end.

FAQ

What should be your first action after receiving a garnishment notice?

This is to be done by immediately filing a claim of exemption with the court. This can put a temporary hold on the garnishment, and you will have the much-needed breathing space to weigh up your options and bargain with your pay not being cut immediately.

Are they really going to take 25% of your paycheck?

No. The garnishment is not allowed to exceed 25 percent of your disposable income (after the deductions required by law) or the number times above 40 times the minimum wage, whichever is less. There is a minimum amount of protection on your take-home pay.

Can declaring bankruptcy stop wage garnishment?

Yes, and very quickly. Filing bankruptcy enacts an automatic stay that legally compels creditors to cease all collection efforts, including wage garnishes, and your case is usually filed within 24 hours.

What are the differences between a wage garnishment and a bank levy?

A wage garnishment is money that is constantly withdrawn from your paycheck. Bank levy is a single-time withdrawal of money from your savings or checking account. They are both potent instruments that creditors employ when they win a judgment.

Are there investments that are safe from garnishment?

Yes. The income is entirely exempt in the state of California, which entails Social Security, SSI, SDI, Veterans benefits, and child support. In case a party that holds your debt garnishes such funds, you can appeal to the court.

800-900-4250

800-900-4250